Value Sharing: Economic Inclusion Requires an Institutional Choice

Social

In the debate on poverty, discussions often focus on how much growth is needed, how much should be transferred, and how much should be redistributed, as if the central challenge were simply to allocate outcomes after the fact. Yet the crucial question is a different one: who participates in the economy before any surplus is created?

Poverty is not merely the absence of income. Above all, it is the absence of access: access to the financial system, productive credit, housing, and the ability to withstand shocks. This is why value sharing should not be viewed simply as redistribution.

The Brazilian experience offers a relevant counterpoint to this perspective. In a country marked by historic inequalities and significant regional disparities, it has become clear that sustainable poverty reduction requires more than isolated transfers. It requires an economic infrastructure capable of connecting public policies, markets, and individuals at scale.

The Role of Institutions in Economic Inclusion

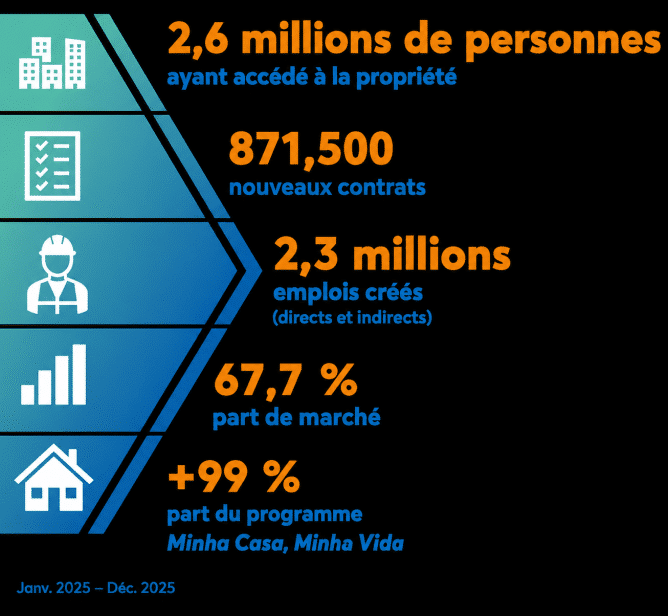

This is where institutions become essential. In Brazil, CAIXA occupies a unique position within this framework. Not only is it one of the country’s largest retail banks, but it also operates simultaneously as a financial institution offering a comprehensive portfolio of products, ranging from productive microcredit to housing finance, in which it holds a leading 67.7% market share. It is also the government’s main public policy operator and serves as a platform for financial and economic inclusion. This combination proves decisive when the objective is to transform rights into real access and to fulfill our purpose of transforming people’s lives.

The payment of benefits to millions of Brazilians is not merely an emergency response by the government to specific situations. It also demonstrates that pursuing inclusion through public policies and institutions with operational capacity, territorial presence, and digital integration is a prerequisite for any large-scale social protection strategy. Beyond simply distributing income, public policies can bring millions of people into the financial system, creating the foundations for more lasting inclusion.

Having a bank account is necessary, but insufficient. The real turning point occurs when access is converted into economic capability: when people begin to save, invest, undertake entrepreneurial activities, and build assets.

Productive Microcredit as a Tool for Economic Empowerment

This is where productive microcredit plays a central, yet often controversial, role. Credit for the most vulnerable populations is frequently viewed as synonymous with indebtedness. However, the Brazilian experience shows that the problem lies not in credit itself, but in its purpose, suitability, and integration with public policies. When directed toward income generation, accompanied by support mechanisms, and integrated into local production chains, it ceases to be a form of financial assistance and becomes an instrument of economic empowerment.

At CAIXA, microcredit reaches both urban and rural entrepreneurs, contributing to the expansion of productive capacity as well as job and income creation throughout the country. By providing loans at affordable interest rates, CAIXA reached an outstanding balance of BRL 1.0 billion in this segment in 2025, benefiting 40,000 individuals and 3,000 businesses.

The same reasoning applies to housing finance. In debates limited to short-term fiscal considerations, housing is often treated as an expense. In practice, however, it is a powerful driver of value sharing. Homeownership provides stability, reduces vulnerabilities, creates a lasting asset, and enhances families’ ability to plan for the future. At the same time, it activates production chains and stimulates regional economies. It is therefore a social policy with profound economic effects.

Brazil’s flagship housing program, Minha Casa, Minha Vida (My House, My Life), was implemented to help address these challenges. Since its creation in 2009, it has helped reduce the country’s housing deficit by 2.8 percentage points, bringing it to its current level of 7.4%.

In 2025, CAIXA reached an outstanding housing finance portfolio of BRL 938.0 billion and granted BRL 246.4 billion in housing loans, helping 2.6 million people gain access to homeownership.

A Virtuous Cycle for the Economy and Society

The result of these actions is the creation of a virtuous cycle. In 2025, the volume of credit granted by CAIXA contributed to the creation of 2.3 million jobs and supported the development of numerous economic sectors by generating demand for construction materials, furniture, and household appliances, thereby stimulating the construction industry and economic growth.

These dimensions cannot be viewed in isolation. Income transfers, financial inclusion, productive credit, and access to housing do not compete with one another. They are interdependent. When coordinated, they enhance the effectiveness of public policies and reduce the need for permanent interventions.

Value Sharing as an Institutional Choice

This framework requires something that neither the market nor the State can provide on their own: scale, continuity, and territorial presence. Institutions with nationwide reach cease to be mere financial intermediaries and become true economic infrastructure, connecting people, territories, and opportunities.

In this sense, value sharing is not merely about redistributing outcomes, but about reducing barriers to entry. It is not a matter of choosing between efficiency and inclusion, but of recognizing that more inclusive economies are, over the medium and long term, more stable and more productive.

The Brazilian experience shows that, without institutions capable of implementing public policies at scale, the promise of inclusive growth is likely to remain rhetorical.

Value sharing is an institutional and strategic choice that takes shape through the expansion of capabilities, the reduction of barriers, and the integration of millions of people into economic life. This agenda can only be sustained when intention becomes public policy, presence becomes access, and action generates real impact.

This is precisely where CAIXA assumes and fulfills its historic role: transforming choices into opportunities, policies into citizenship, and development into tangible results in people’s daily lives, thereby bringing its purpose of transforming lives into reality.