Biodiversity on the brink: How nature markets may avert an irreversible collapse

Environnement

Towards an irreversible collapse of biodiversity

Chainsaws echo through the Amazon by day, and wildfires crackle by night, clearing the forest for cattle and crops. Mangroves rot under surging seas in Manila Bay, and a once-vibrant reef drifts lifeless beneath the ocean’s wave. In the time it took to read this sentence, our planet has lost an estimated 10 football pitches of tropical forest[1] and many thousands of pollinating insects that once stitched food chains together.

Nature’s degradation is not merely ecological – it is profoundly economic. Costanza et al. (1997) estimated that the value of ecosystem services provided by the biosphere ranges from one to three times the global GDP. Moreover, forests are home to over half of the planet’s land animal and plant species and directly support millions of people by providing food, income, and shelter. With half of global GDP dependent on healthy ecosystems, biodiversity collapse is an economic crisis waiting to happen (WEF, 2022).

Traditional market solutions fall short

Existing mitigation efforts have largely focused on carbon emissions, leading to the widespread adoption of carbon markets as a financial instrument for pricing and reducing greenhouse gas emissions. More recently, biodiversity and nature markets have been proposed as complementary mechanisms to carbon markets, with the aim of channeling private finance into conservation and restoration efforts. Indeed, many nature-based carbon projects – such as reforestation, afforestation, and mangrove restoration – deliver both carbon sequestration and biodiversity co-benefits (Kedward et al., 2023). However, these projects are typically valued and traded based on the carbon they capture, measured in tons of CO₂-eq, while biodiversity is treated as a secondary benefit, leading only to a modest price premium.

This approach has proven fundamentally inconclusive for two key reasons. First, such voluntary carbon markets are increasingly dysfunctional and in decline due to persistent issues of additionality, leakage, permanence, baseline accuracy, and traceability (Cantillon and Slechten, 2024). For instance, recent investions have exposed serious flaws in voluntary carbon markets, revealing that over 90% of rainforest carbon offsets certified by Verra, a major standard-setting organization, were ineffective[2]. These scandals exposed deep systemic issues that undermine market credibility. At the same time, efforts to fix the system by tightening certification requirements do not address the core flaw: carbon credits are one-off transactions that shift long-term biophysical risks onto project developers rather than investors.

Figure 1: Forest- stylized age profile of a stock and flow of CO2 and biodiversity. Source: Cantillon et al. (2025).

Second, bundling carbon and biodiversity into a single category causes confusion and further damages the market credibility as carbon and biodiversity issues are fundamentally different. Indeed, depending on the intervention, carbon sequestration or storage may be positively, negatively, or not correlated at all with biodiversity conservation or restoration. For instance, while monoculture afforestation initiatives may help mitigate climate change, they often harm biodiversity (Kedward et al., 2023). Moreover, carbon and biodiversity follow different stock-versus-flow dynamics, as illustrated by the age profile of a forest’s carbon and biodiversity production (Figure 1).

A young, naturally regrowing forest is highly effective at removing carbon from the atmosphere (carbon flow), but its biodiversity stock remains relatively low. Conversely, a mature forest supports a rich biodiversity stock but is less efficient at capturing new carbon because new growth is roughly balanced by decomposition, which releases carbon. However, mature forests act as important reservoirs for permanent carbon storage (carbon stock). Thus, while young forests are especially valuable for their carbon uptake, mature forests are important both for their stored carbon and the biodiversity they sustain.

A new market design for nature-based provision

In Cantillon et al. (2025), we fundamentally rethink biodiversity financing. Current credits sold on the voluntary markets monetise annual flows (tonnes of CO₂, hectares restored) but ignore permanence: once sold, the buyer has little incentive to keep financing the conservation of the forest that underwrites the certificate. Thus, we flip the unit of trade: we propose that jurisdictions would issue nature shares in large-scale, nature-positive projects. A nature share is a claim on the stock of an ecosystem which pays out carbon and biodiversity dividends over time. Crucially, dividends are prudently managed to account for the inherent impermanence of ecosystems, ensuring a buffer against future environmental shocks. This creates incentives for long-term stewardship rather than short-term transactional gains. If fires, pests or political turmoil reduced the underlying stock, future dividends would fall, in the same way as equity investors bear corporate downside risk.

The proposed nature shares respect the carbon and biodiversity stock-versus-flow dynamics: early-stage projects may use most dividends to build risk reserves, whereas mature reserves can begin steady payouts.

Zone de Texte: Figure 2: The design of nature-based equity market. Source: Cantillon et al. (2025).

The market functioning is illustrated in Figure 2: juristictions will sell nature shares on a primary market, which operates through a crowdfunding-inspired model, where projects list their

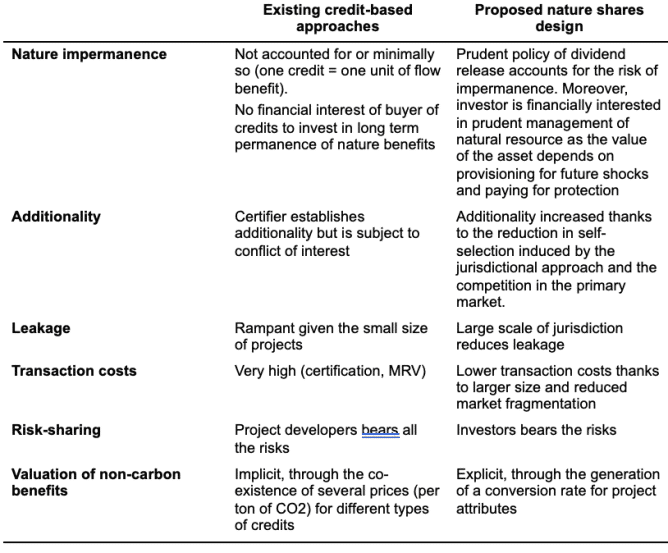

Table 1: Comparison between existing approaches and the proposed market design. Source: Cantillon et al. (2025).

attributes transparently. Investors allocate funds based on their preferences, driving project pricing through market demand. Projects receiving more investor interest see their share prices rise, clearly signaling market priorities. Additionally, a secondary market enables investors to sell shares if their circumstances change, ensuring liquidity and flexibility. This market is supported by standardized indicators and transparent pricing from the primary market, facilitating easy trading and reliable valuation.

The strategic advantages of nature shares

The shift from transactional credits to a share-based investment approach has four knock-on effects (see Table 1). First, since dividends can be withheld and re-allocated to emergency replanting, non-permanence is internalised rather than wished away. Second, jurisdiction-wide projects spread fixed monitoring, reporting and verification costs over thousands of hectares, slicing today’s 40% minimum intermediation margin. Third, we propose that a primary “crowdfunding” exchange prices each project, so that jurisdictions posting inflated minimum prices risk funding failure. Fourth, primary-market clearing prices reveal investors’ willingness to pay for attributes such as Indigenous stewardship or watershed protection, replacing today’s murky price-premia on “charismatic” credits.

The future ahead

Earlier mitigation efforts have largely focused on the supply side, simply considering the demand as ‘granted’. However, the history of the Voluntary Carbon Market has thought us how credits oversupply results in prices declines and low market credibility. To avoid this faith, we propose regulatory mandates that pension and investment funds include biodiversity shares. This approach leverages the immense financial power of institutional investors, creating consistent, large-scale demand.

In conclusion, nature markets may avert the current biodiversity collapse. The innovative, share-based market mechanism proposed by Cantillon et al. (2025) provides an actionable economic model aligned directly with ecological sustainability. By fundamentally restructuring how we finance biodiversity, we can ensure that economic incentives reinforce long-term ecological stewardship, thereby preventing an irreversible ecological collapse.

References

Cantillon, E., Lambin, E., and Weder di Mauro, B. (2025). Designing and scaling up nature-based markets. Part of the Third Paris Report: Accelerating the transition and protecting nature in EMDEs. CEPR Press.

Cantillon, E., and Slechten, A. (2024). Market Design for the Environment (No. w31987, revised August 2024). National Bureau of Economic Research.

Costanza, R., d’Arge, R., De Groot, R., Farber, S., Grasso, M., Hannon, B., … and Van Den Belt, M. (1997). The value of the world’s ecosystem services and natural capital. Nature, 387(6630), 253-260.

FAO – Food and Agricalture Organization – and UNEP – United Nations Environmental Program (2020). The State of the World’s Forests 2020. Forests, biodiversity and people. (https://doi.org/10.4060/ca8642en)

Kedward, K., Ryan-Collins, J., and Chenet H. (2023). Biodiversity loss and climate change interactions: financial stability implications for central banks and financial supervisors. Climate Policy, 23:6, 763-781.

WEF – World Economic Forum (2020). Nature Risk Rising: Why the Crisis Engulfing Nature Matters for Business and the Economy. (https://www.weforum.org/publications/nature-risk-rising-why-the-crisis-engulfing-nature-matters-for-business-and-the-economy)

[1] Each year, the world clears around 10 million hectares of forest (FAO, 2020). That translates to 0.32 ha every second, or 5.44 ha in 17 seconds, i.e. the time an average reader needs to move through the opening lines. A regular football pitch occupies between 0.4 ha (FIFA minimum dimensions) and 0.7 ha (FIFA World-Cup standard). Dividing 5.44 ha by that range yields 7.77 – 13.6 pitches; rounding to the midpoint gives the ≈10 figure used above. The image is dramatic, but the arithmetic is conservative.

[2] https://www.theguardian.com/environment/2023/jan/18/revealed-forest-carbon-offsets-biggest-provider-worthless-verra-aoe [Accessed on Jun 24, 2025.]