A soft power of financial markets?

Soft power is the ability to co-opt rather than coerce, shaping the preferences of others through appeal and attraction. Usually, the concept of soft power is associated with culture and with human and political values, including international solidarity and caring for global public goods.

We often think soft powers as positive tools even if history is rich of examples of negative soft powers.

Credibility is at the roots of the potential use of soft powers: we should take note that during our information age there is a lack of credibility, both at the private and at the state levels.

According to Joseph Nye, in 1990 the US were “bound to lead” the world, precisely for their soft powers. Lately, it would be difficult to state the same.

In this note I want to make a point on the relevance of finance as a soft power.,

Economics and soft power

Usually, economics is not considered a soft power; on the contrary, economic incentives are thought as hard power tools, along with military force. Soft power sceptics would state that international relations respond only to force and/or economic conveniences.

However, traditional soft powers have a reciprocal relationship with economic conditions that reinforces their positive or negative effects. In one direction, positive (negative) soft powers improve (deteriorate) economic welfare in many ways. In the other direction, sound and efficient economic markets and conditions can exert favourable influences in international relations forming sustainable bases for the success of fruitful cultural dialogues and value-based cooperative policies.

Freedom, widely defined, as well as the rule of law, i.e. rule-based relations of various sorts, are crucial soft power tools but are also essential requirements for the efficiency of markets and for an allocation of resources that favours sustainable growth.

Neither China nor Sandi Arabia are good examples of freedom and of the rule of law; however, their use of economic soft power as a tool to improve their economic integration with the rest of the world is explicit and evident. I see many reasons to avoid discarding the idea that favouring their efforts in these directions, also by allowing them to increase their roles in international institutions and global governance, could accelerate their steps towards freedom and democracy, away from some arbitrariness of autocracies.

Let me now narrow the focus: from economics to financial markets.

Finance

Financial markets have a very special impact on international relations as their international expansion and intrusiveness are unstoppable. Even when the growth of indices of economic globalization slow down, financial globalization keeps growing. Sometimes its shape worsens, decreases its efficiency and its transparency, but keeps growing. Digital finance and AI reinforce this global pervasiveness of finance.

Therefore, to the extent that finance can convey some soft-power, that power will be spreading across frontiers.

Finance is often accused to favour the strong and the big, without offering adequate opportunities to weaker and smaller agents. Moreover, the strong ones are always suspected to influence the shaping of financial rules as well as their supervision, without regard to the common good. Information asymmetries are well known characteristics of financial markets and can hurt trust, which is the basis of efficient market making. And so on: a long list of bad aspects of finance can be well grounded in reality and in the results of economic research.

However, these aspects, per se, do not prevent to rely on financial markets as soft powers, able to increase international cooperation for the common good. These defects of finance depend on the inadequacy of financial regulation and supervision that, if rendered adequate, could come to the point of leveraging precisely on the caring for these aspects to diffuse the values that support the soft power of financial markets.

Cooperative efforts to level the financial playing field can be conducive to an increasing respect for targeting better balanced economic conditions. Promoting transparency of financial markets and operations helps valuing transparency, truth and trust, in many different economic, political and social instances and institutions. Defending the independence of financial regulators and supervisors can help to stress the importance of the division of powers in a true democracy. Promoting competition and international integration in finance is both a condition and a stimulus to strengthen the soft power of openness and fairness.

All this applies to economic relations in general; however, let me say that finance seems particularly fit for acting as a soft power at the international level as it is somewhat less relationship based, more standardized, and because its qualities – as well as its defects – tend to quickly spread around the world and show that global cooperation is essential for the common good.

Europe

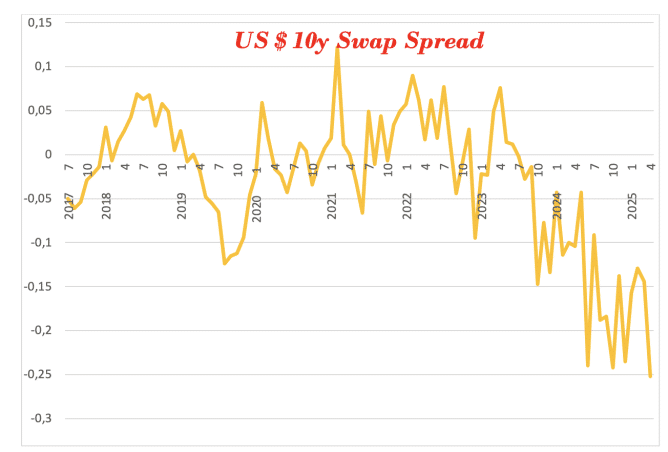

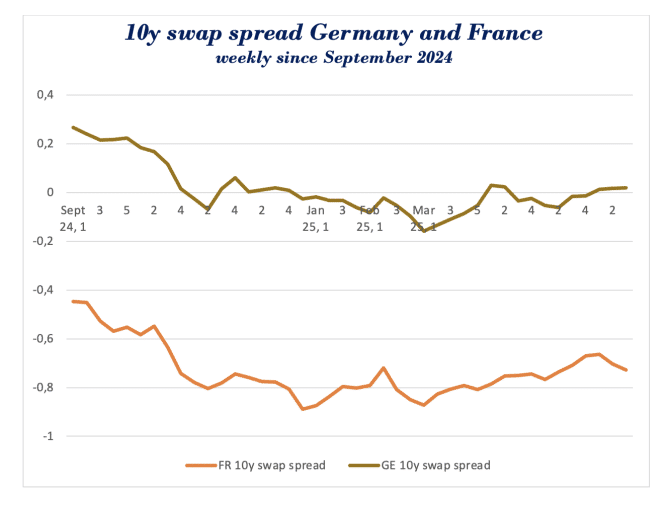

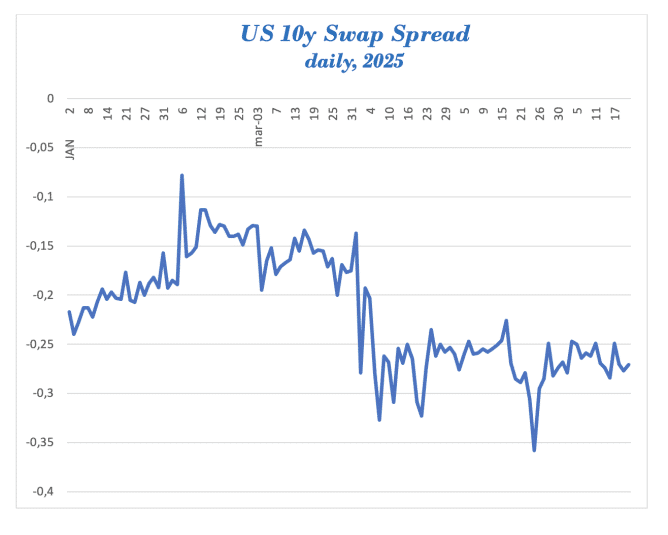

In a period of dangerous crisis of the soft power of US financial markets, could Europe do something to increase its soft power also in the financial field? The answer is yes; the inspection of swap spreads on government securities (see the figure below), that are inversely related to country risks, confirms that perceived country risks are moving against the US and in favour of European debtors. However, the road to make finance a soft power of Europe is long and steep.

This is not the occasion to propose a well-organized recipe to make European financial markets a crucial tool to improve global international relations and cooperative policies. Let me simply mention two lines of action that, in fact, are already in the EU agenda, even if in too cautious, slow and timid ways.

First, Europe should start a cultural and political battle to abandon the idea that different financial rules and different financial supervisors in different countries can bring any sustainable and fair economic advantage to individual member states. On the contrary: offering a unified financial market to the world would be a formidable soft power, helping all our international relations and multilateral global institutions. The aim should not be to compete with the dollar market nor to substitute it: there is plenty of room to complement it. Even if, in the short run, the euro-based market could act as a partial substitute for some weakening of dollar-based activities.

10Y SWAP SPREADS US, GERMANY AND FRANCE10Y SWAP SPREADS US, GERMANY AND FRANCE

More country risk decreases the spread

Second, Europe should plan for a significant reshaping of the risk-bearing capacity of European finance, keeping very strong rules and supervisions for certain parts of financial markets and some crucial zero-risk operations, while gradually pushing other parts toward freer risk bearing. Household, savers, firms, intermediaries must cease to be thought as risk minimizing actors and stop being regulated accordingly.

With good risk free and low risk assets, trustable authorities and adequate financial transparency, all markets agents must be in the position to find their preferred risk-expected return mixture and pay, when necessary, the price of a bad outcome of their chosen risk taking.

After all, risk bearing has been for long the most important soft power of US financial markets. Europe could target a somewhat different risk-bearing atmosphere with a somewhat different regulation, but the globally beneficial, soft power of its financial markets requires a cultural and regulatory jump in the risk bearing capacity of its finance, which would also be of help for improving the allocation of resources.